Accounting Updates for Southern Gas Association Accounting

& Financial Executives Conference

Bob

Jensen at Trinity

University

Bob

Jensen's threads on accounting theory are at http://www.trinity.edu/rjensen/theory.htm

Systemic Problems of Accounting and Auditing ---

http://www.trinity.edu/rjensen/FraudConclusion.htm

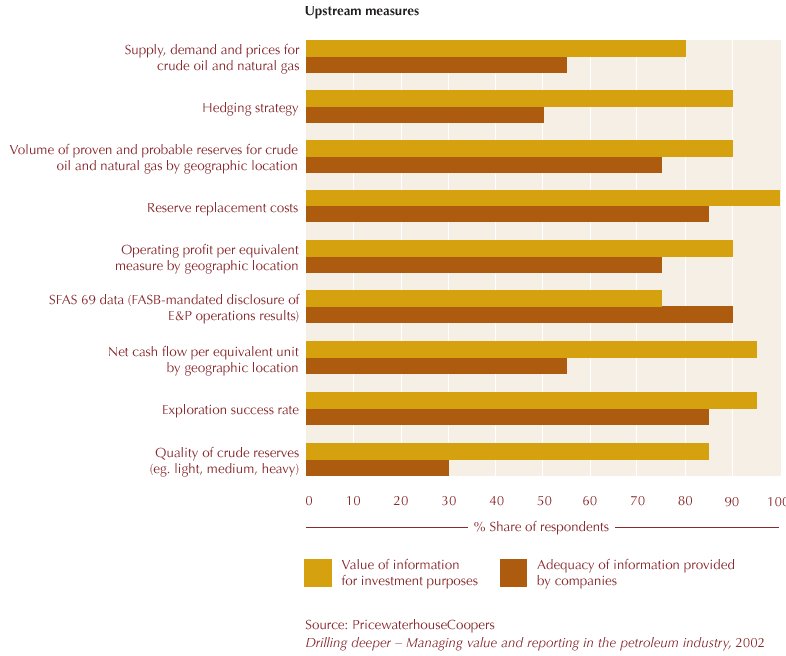

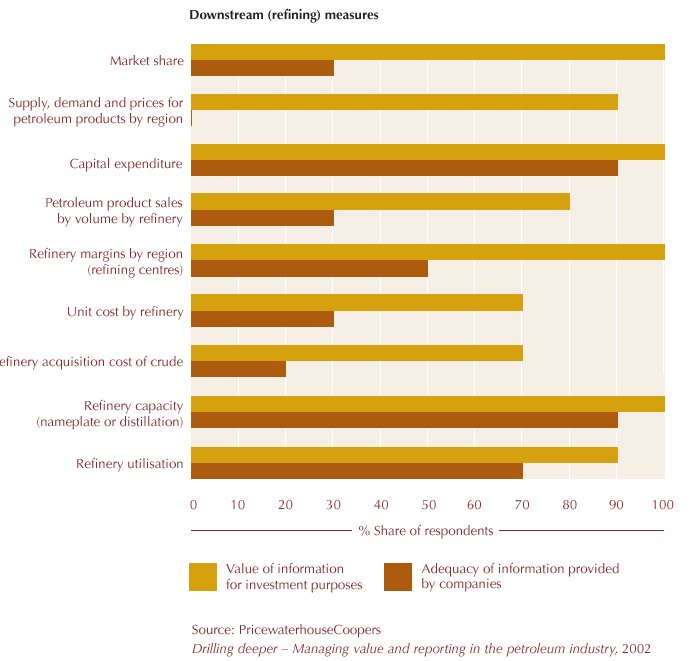

Equity Valuation in the Oil and Gas Industry

DRILLING DEEPER: MANAGING VALUE AND REPORTING IN THE

PETROLEUM INDUSTRY,

A Special Report from PricewaterhouseCoopers (PwC), 2002 --- http://www.pwc.com/images/gx/eng/about/ind/petro/drilling_deeper.pdf

Executive Summary

The traditional, predominantly financial,

indicators used to measure corporate performance no longer meet the

needs of the global capital markets. They do not tell a company’s

full story and are not adequate to deliver true insight into its

capacity to grow, adapt and change. Our survey of petroleum companies,

investors and analysts, demonstrates the case for more comprehensive

reporting.

Eighty per cent of petroleum companies in the

survey believe their share price falls short of their company’s true

value. But the reporting practices of petroleum companies in turn fall

short of what investors and analysts say they need to assess companies

for investment purposes. Investor feedback revealed that for about

three of every five indicators they highlight as having particular

value in assessing companies, the information flow from companies is

significantly below what they need.

Only a few of the indicators fall into the

category of traditional financial reporting. Instead, they cover

ground such as the geopolitical environment, strategic direction and

quality of management. Investors also express a desire for information

to be better-segmented in the upstream and downstream sectors.

The survey indicates that petroleum companies

need to work more effectively to achieve their investor dialogue

goals. More than half of companies (52 per cent) believe they work

proactively to initiate contact or maintain continuous dialogue with

investors, yet only 14 per cent of investors characterised petroleum

companies in this way.

A shift to more comprehensive reporting will

help petroleum companies move away from the treadmill of continuous

focus on short-term earnings. Investor cynicism about short-term

earnings runs high. Three-quarters of investors feel that petroleum

companies have considerable discretion on earnings figures, yet this

leeway is firmly refuted by companies themselves.

A move to wider reporting is seen by

companies, investors and analysts as likely to lead to tangible gains

for companies. Reduced share-price volatility, increased valuations,

more long-term investment, a lower cost of capital and greater

management credibility are among the benefits of better disclosure

cited by a majority of those surveyed.

Value indicators – Responses

of analysts for the indicators in the

general, upstream E&P and downstream refining sectors.

|

Value indicators – Responses

of analysts for the indicators in the

general, upstream E&P and downstream refining sectors.

|

|

KMPG's eValuation

"Services Calculate Net ROI Consulting firms update traditional business

metrics for Internet" By Chuck Moozakis, Internet Week, August 24, 2000 ---

http://www.internetwk.com/lead/lead082400.htm

Calculating Net ROI

The fledgling oil and

gas exchange PetroCosm knew it needed more than the backing of giants Chevron

and Texaco to win over customers and suppliers. Even more important was the

ability to demonstrate clear financial benefits for participants.

In the months leading

up to its July launch, PetroCosm worked with consulting firm KPMG to develop a

return-on-investment (ROI) model that would help potential customers make the

case for participating in the exchange.

PetroCosm used a new

KPMG service dubbed eValuation--announced last week--that takes into account

traditional ROI variables, such as up-front development costs, as well as more

Internet-centric variables, such as the additional sales that can be derived

by participating in a wide range of online marketplaces. It also factors in

the cross-company ramifications of Internet supply chains and how customers

and suppliers can also benefit.

"We were able to

come up with a business case that said this is a profitable business" for

both suppliers and PetroCosm's founding members, said PetroCosm controller Rod

Starr. "It sounds straightforward enough, but one of the great challenges

is that there are no existing models to gauge ROI."

Armed with results

from the ROI study that indicated the type of cost savings prospective members

could realize by participating in a B2B exchange, PetroCosm has been able to

sell prospective participants on the possibility of trimming anywhere from 5

percent to 20 percent of their procurement costs by joining the marketplace,

Starr said. --Chuck Moozakis

Read the rest: http://www.internetwk.com/lead/lead082400.htm

How might companies

present their financial performance in a better light?

Bob Jensen's Threads on "Core Earnings" Theory and Implementation

--- http://www.trinity.edu/rjensen//theory/00overview/CoreEarnings.htm

Bob Jensen's Threads on Pro Forma Earnings --- http://www.trinity.edu/rjensen//theory/00overview/theory01.htm#ProForma

The New York

Yankees today released their 4th Quarter 2001 pro forma results. Although

generally accepted scorekeeping principles (GASP) indicate that the Yankees lost

Games 1 and 2 of the 2001 World Series, their pro forma figures show that these

reported losses were the result of nonrecurring items, specifically

extraordinary pitching performances by Arizona Diamondbacks personnel Kurt

Schilling and Randy Johnson. Games 3 and 4 results, already indicating Yankee

wins, were not restated on a pro forma basis.

Ed Scribner, New Mexico State

Equity Valuation

Bob Jensen's Threads on Return on Business Valuation, Business Combinations,

Investment (ROI), and Pro Forma Financial Reporting --- http://www.trinity.edu/rjensen/roi.htm

|

Questrom vs. Federated Department Stores, Inc.: A Question of Equity

Value," by Gary Taylor, William Sampson, and Benton Gup, Issues in

Accounting Education, May 2001, pp. 223-256.

This is perhaps the best short case that I've ever read. It will

undoubtedly help my students better understand weighted average cost of capital,

free cash flow valuation, and the residual income model. The three student

handouts are outstanding. Bravo to Taylor, Sampson, and Gup. If you

subscribe to the electronic option of the American Accounting Association, you

can download the case from http://aaahq.org/ic/browse.htm

The market value

represents the firm’s stock price at a given point multiplied by the number of

shares outstanding. The intrinsic value

of the firm is the present value of the forecasted payoffs of income, cash flow,

or other economic variables to the stockholder; thus, the intrinsic value

represents the value implied by avail-able information. The intrinsic value is

the theoretical value of the firm based on any one of a variety of valuation

methods such as free cash flow,

residual income, or dividend

discount. Consequently, wide variation can exist in

estimates of a firm’s intrinsic value.

During the 1980s, a significant amount of research

suggested that financial markets are informationally efficient. However, in

recent years, research has re-vealed many market imperfections. Size and

seasonality effects temper the assumption that stocks are fairly priced at any

given time. In addition, Wall Street spends a considerable amount of time and

money on identifying “mispriced stocks,”

Market Value

Market value is only indirectly affected by limited and/or misleading financial

reports. Traders and investors can look at all other sources of

information setting bid and ask prices. However, only a small proportion

of shares are usually traded and these seldom reflect the value of enormous

blocks of equity, especially blocks that provide ownership control of

management. Also, daily stock prices are heavily influenced by general

market conditions and trends that may be poorly correlated with changes in value

in a particular company. Also daily stock prices are impacted upon by

accounting data news releases that are subject to all the limitations of

accounting data used in computing intrinsic values.

Intrinsic Value

Intrinsic value suffers most from more direct reliance upon what

accountants report in the way of earnings, cash flows, and account

balances. The main limitation is the valuation impact of items not

accounted for such as intellectual capital, quality reputation, brand

recognition, political power/connections, monopoly power, and other

intangibles. Another major problem is that management compensation

contracts contribute to misleading and/or fraudulent manipulation of the

accounting numbers. Further complications include impacts of

extraordinary items in financial statements and early extinguishment of

debt. Enormous problems arise from complicated and obscure

measurement and disclosures under such unfathomable accounting standards

like FAS 133 on Accounting for Derivative Financial Instruments and

Hedging Activities. Many disclosure footnotes such as the infamous

Footnote 16 of the Enron 2000 annual report cannot be understood by top

experts --- http://www.trinity.edu/rjensen/fraud.htm#Senator

- Discounted Dividend (DD)Valuation:

In theory, the best economic value is the present value of all

future cash flows (dividends) on each share of common stock.

Since many firms do not pay dividends or pay miniscule dividends,

the ability to pay a dividend must be used as a surrogate for

dividends. This in turn leads to the FCF surrogate described

below.

- Free Cash Flow (FCF)

Valuation:

"Free cash flow" is the amount of cash remaining from

operations after cash is used

for new investments. It is the cash theoretically avail-able to

pay bondholders and shareholders. It is calculated as the sum of

"net cash provided

from operating activities," after adding back after-tax net

interest payments, less

(plus) "cash used for (generated from) investing

activities." The resulting amount

is the cash available to pay bondholders or shareholders, i.e.,

"free cash

flow."

- FCF is not a true measure of value created since cash outflows

for investing activities reduce FCF. However, as long as the

company is not investing in negative NPV projects, investing

activities should increase firm value. Problems with the FCF

model are evident for firms whose FCFs have not reached a steady

state. For these firms, it is difficult to predict the timing of

future investing activities, making it difficult to predict

expected future free cash flows. If these firms are successful,

they will ultimately incur positive free cash flows, but only in

the future, when returns from their investment are

realized.

- Wal-Mart illustrates the problems associated with using the

FCF model to estimate the intrinsic value of a firm whose FCFs

have not reached a steady state. From 1988 through 1996,

Wal-Mart’s FCFs were positive only in 1989. The negative FCF

amounts during these years were due to the large outflows of

cash used to expand its retail stores; these outflows for

investing activities exceeded Wal-Mart’s operating cash flow.

Despite its negative FCFs, Wal-Mart’s price per share

increased from $6.875 in 1988 to $20.375 in 1996. In addition,

Wal-Mart notes in its 2000 annual report plans to expand in

international markets, thereby making additional negative free

cash flows likely for the foreseeable future. Yet the price per

share continues to increase.

- Residual Income (RI) or "Abnormal Earnings"

Valuation:

“Residual Income” is the earnings above “normal earnings.”

“Normal earnings” are the required earnings expected by

investors, given the cost of capital, and is calculated by

multiplying the beginning-of-the-period book value of equity (Bt–1

) by the firm’s cost of capital (r). Mathematically, residual

income for period t is from forecasted eps estimates (fepst

– rBt–1 ) where fepst is forecasted

earnings for period t. Residual earnings are also called “abnormal

earnings.”

Residual Income Model:

The “Residual Income” (RI) model is a valuation tool that is

derived directly from the discounted dividend model. The RI model

estimates intrinsic value by looking at both “stocks” (balance

sheet equity amounts) and “flows” (earnings). The RI model

estimates a firm’s total equity value as a function of the book

value of common equity and the present value of residual income. The

mathematical relationship between per-share forecasted earnings,

share price, and book value is: P0 = B0 +

Sum[(1 + r) –t (feps t – rB t–1 )], where P0

and B0 represent today’s price per share and book value

per share of equity, respectively. Cost of capital is defined as r

and forecasted earnings per share as “feps.”

Federated's

Valuation Estimates Using the Free Cash Flow (FCF) Model

Subtracting Deferred Taxes

Table 1

on Page 251 when the share price on January28, 1995 was $18.625

| |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

| Discount

Rate |

No

Perpetuity

1995-1999 |

Perpetuity |

Growing

in Perpetuity |

| 5% |

$(30.80) |

$93.22 |

$279.26 |

| 10% |

$(33.15) |

$18.34 |

$40.40 |

| 15% |

$(35.07) |

$(

6.34) |

$

0.84 |

|

Federated's

Valuation Estimates Using the Residual Income (RI) Model

Table 2

on Page 252 when the share price on January28, 1995 was $18.625

| |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

| Discount

Rate |

No

Perpetuity

1995-1999 |

Perpetuity |

Growing

in Perpetuity |

| 5% |

$23.33 |

$62.64 |

$121.59 |

| 10% |

$19.37 |

$27.24 |

$30.61 |

| 15% |

$16.21 |

$15.89 |

$18.81 |

|

The share price on April 3, 2003 was $28.50. There are no

dividends.

|

FASB Standards of Particular Interest

Statement No. 148

Accounting for Stock-Based Compensation—Transition and Disclosure—an

amendment of FASB Statement No. 123

(Issue Date 12/02)

[Summary] [Status]

Statement No. 147

Acquisitions of Certain Financial Institutions—an amendment of FASB

Statements No. 72 and 144 and FASB Interpretation No. 9

(Issue Date 10/02)

[Summary] [Status]

Statement No. 146

Accounting for Costs Associated with Exit or Disposal Activities

(Issue Date 6/02)

[Summary] [Status]

Statement No. 145

Rescission of FASB Statements No. 4, 44, and 64, Amendment of FASB

Statement No. 13, and Technical Corrections

(Issue Date 4/02)

[Summary] [Status]

Statement No. 144

Accounting for the Impairment or Disposal of Long-Lived Assets

(Issue Date 8/01)

[Summary] [Status]

Statement No. 143

Accounting for Asset Retirement Obligations

(Issue Date 6/01)

[Summary] [Status]

Statement No. 142

Goodwill and Other Intangible Assets

(Issue Date 6/01)

[Summary] [Status]

Statement No. 141

Business Combinations

(Issue Date 6/01)

[Summary] [Status]

Statement No. 140

Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities-a replacement of FASB Statement No. 125

(Issue Date 9/00)

[Summary] [Status]

Statement No. 139

Rescission of FASB Statement No. 53 and amendments to FASB Statements No.

63, 89, and 121

(Issue Date 6/00)

[Summary] [Status]

Statement No. 138

Accounting for Certain Derivative Instruments and Certain Hedging

Activities-an amendment of FASB Statement No. 133

(Issue Date 6/00)

[Status]

Statement No. 137

Accounting for Derivative Instruments and Hedging Activities—Deferral of

the Effective Date of FASB Statement No. 133—an amendment of FASB Statement

No. 133

(Issue Date 6/99)

[Status]

Statement No. 136

Transfers of Assets to a Not-for-Profit Organization or Charitable Trust

That Raises or Holds Contributions for Others

(Issue Date 6/99)

[Summary] [Status]

Statement No. 135

Rescission of FASB Statement No. 75 and Technical Corrections

(Issue Date 2/99)

[Summary] [Status]

Statement No. 134

Accounting for Mortgage-Backed Securities Retained after the

Securitization of Mortgage Loans Held for Sale by a Mortgage Banking

Enterprise—an amendment of FASB Statement No. 65

(Issue Date 10/98)

[Status]

Statement No. 133

Accounting for Derivative Instruments and Hedging Activities

(Issue Date 6/98)

[Summary] [Status]

Statement No. 132

Employers' Disclosures about Pensions and Other Postretirement

Benefits—an amendment of FASB Statements No. 87, 88, and 106

(Issue Date 2/98)

[Summary] [Status]

Statement No. 131

Disclosures about Segments of an Enterprise and Related Information

(Issue Date 6/97)

[Summary] [Status]

Statement No. 130

Reporting Comprehensive Income

(Issue Date 6/97)

[Summary] [Status]

Further disconnects income statement from the balance sheet

Free from the FASB

Accounting for Stock-Based Compensation: A Comparison of FASB Statement No. 123,

Accounting for Stock-Based Compensation, and Its Related Interpretations,

and IASB Proposed IFRS, Share-based Payment (Invitation to Comment)

November 18, 2002

(Comment period ends February 1, 2003)

[Download]

--- http://www.fasb.org/draft/itc_intropg_stock_based_comp.shtml

Note that adjustments for many more companies are available in the "Core

Earnings" revisions from Standard and Poors at http://www2.standardandpoors.com/NASApp/cs/ContentServer?pagename=sp/Page/PressSpecialCoveragePg&b=5&r=1&s=3&ig=1026841911315

I also created the shorter URL --- http://snurl.com/CoreEarnings

In response to growing concern about companies

earnings reports, Standard & Poor’s has introduced a new methodology

called “Standard & Poor’s Core Earnings.” The ultimate goal is to

lead investors and analysts to a consensus on earnings calculations, and bring

more transparency and consistency to earnings analysis and forecasts.

Bob Jensen's threads on these this controversy can be found at http://www.trinity.edu/rjensen/theory/sfas123/jensen01.htm

New

FASB Now Expects to Issue the proposed limited-scope statement, Accounting for

Certain Financial Instruments with Characteristics of Both Liabilities and

Equity, in the second quarter of 2003

Project Update --- http://www.fasb.org/project/liabeq.shtml

RECENT DEVELOPMENTS

- The Board issued two FASB Exposure Drafts, Accounting

for Financial Instruments with Characteristics of Liabilities, Equity, or

Both, and Proposed Amendment to FASB Concepts Statement No. 6 to

Revise the Definition of Liabilities, on October 27, 2000. (Copies of

both Exposure

Drafts may be downloaded from this Website, along with the

analysis of the proposed Statement’s impact on EITF consensuses.) The

Board began its redeliberations of the issues in the Exposure Drafts in

the light of comments received on those Exposure Drafts, in December 2001,

starting out with issues addressing separation of compound instruments.

Accounting for Financial Instruments with Characteristics of

Liabilities, Equity, or Both (Proposed Statement of Financial

Accounting Standards)

October 27, 2000

Exposure Draft

[Download] --- http://www.fasb.org/draft/ed-fi.pdf

EITF

Analysis --- http://www.fasb.org/draft/eitfliabeq.shtml

- On June, 5, 2002, before resolving the separation

issues, the Board decided to change the order of issues it would address

in its redeliberations so that it could immediately address concerns

relating to financial instruments embodying obligations that could be

settled by the issuance of an entity’s own shares. After redeliberating

those issues, on November 13, 2002, the Board decided to issue a

limited-scope Statement addressing the following instruments:

- Financial instruments embodying, or indexed

to, an obligation to repurchase an issuer’s equity shares that

requires or could require settlement by transfer of assets

- Mandatorily redeemable instruments

- Financial instruments embodying an obligation

that the issuer must or could settle by issuing a variable number of

its equity shares if the monetary value of the obligation is based

solely or predominantly on (a) a fixed monetary amount known at

inception, (b) variations in something other than the fair value of

the issuer’s equity shares, or (c) variations in the fair value of

the issuer’s equity shares, but in the direction opposite to those

variations.

- The Board decided to issue a final Statement. The

Board believes that rapid issuance of the Statement, even though

separation and conceptual issues affecting other instruments are not yet

resolved, is needed to provide timely and necessary guidance for certain

troublesome instruments.

April 2, 2003 message from Terry Bechtel [bechtelt@nsula.edu]

Dr. Jensen,

I would suggest that the use of 3-D and 4-D seismic is of significance. I am

told that the probability of success when an oil well is drilled is now about

75%. In the past successful wells occurred about one time in nine and even less

frequently in wildcat situations. It would seem to me that this might have

implications regarding the use of the full-cost versus the successful efforts

methods of accounting. I hope that you find this useful. Also please say hello

to Petrea for me as we are old friends.

Terry B.

Comparisons of International IAS Versus FASB Standards --- http://www.deloitte.com/dtt/cda/doc/content/pocketiasus.pdf

SEC Proposed Rule: on Disclosure in Management's Discussion and Analysis

about the Application of Critical Accounting Policies --- http://www.sec.gov/rules/proposed/33-8098.htm

(Relates to the older FR-60)

- Basic information needed to understand estimates, such as the underlying

methodology and assumptions

- Effect of estimates on financial presentation

- Sensitivity of the financial results to changes in the estimates or their

underlying assumptions

- Statement as to whether or not management discussed the development,

selection, and disclosure of the estimates with the company’s audit

committee

- Requires management to make assumptions about matters that are “highly

uncertain” at the time the estimate is made, and it must be an estimate

for which different estimates reasonably could have been used, or changes

are reasonably likely to occur, that would have a material impact on

financial results

- Examples

- Revenue recognition policies and methods

- Related party transactions

- Valuation of investments

- Debt and debt covenants

- Deferred tax assets

- Commitments and contingencies

- Oil and gas reserves (Plans to develop PUDs, Proved Undeveloped

Reserves)

- Impairment of oil and gas properties (significance of probable/

possible reserves)

What's Right and What's Wrong With (SPEs),

SPVs, and VIEs --- http://www.trinity.edu/rjensen//theory/00overview/speOverview.htm

FIN

46

Revised

FIN 46 Interpretation of Accounting Research Bulletin No. 51, Consolidated

Financial Statements,

Consolidation of VIEs on the basis of risk rather than voting control

From the January 17, 2003 FEI Express

Those

FEI members whose companies have November 30 or December 31 fiscal year-ends

need to take a close look at FASB Interpretation No. 46, Consolidation of

Variable Interest Entities, as soon as possible for two reasons: (1) FIN 46

has disclosure requirements that become effective for financial statements

issued after January 31, 2003; (2) FIN 46 applies to all types of

unconsolidated entities (e.g., joint ventures, partnerships, cost basis

investments, etc.). For those who have not followed this project closely, FIN

46 could affect your company's financial statements even if it has no

involvement with so-called "special purpose entities" (SPEs). The

following is a brief synopsis of the rule. The complete document is available

now at the FASB's web site at: http://www.fasb.org/interp46.pdf.

Transactions that will come

under FIN 46 scrutiny include the following:

-

off-balance-sheet

R&D ventures,

-

synthetic leases,

-

asset-backed commercial

paper,

-

collateralized debt

obligation, and

-

exploration ventures,

-

others.

FR-61 SEC Disclosure in Management's Discussion and Analysis About

Off-Balance Sheet Arrangements, Contractual Obligations and Contingent

Liabilities and Commitments

- Off balance sheet arrangements (SPEs, VIEs)

- Contractual obligations and commercial commitments

- Energy trading activities

- Related party transactions

FAS 133 and IAS 39 --- Accounting for Financial Instruments Derivatives

and Hedging Activities

- Fair Value Hedges (Inventory On Hand, Firm Commitments, Tolling, Capacity,

Transportation Agreements, Fixed Rate Debt)

- Cash Flow Hedges (Forecasted Transactions Other Than Derivatives, Interest

Rate Risk)

- Normal Purchases, Normal Sales

- Terminating cash flow hedges is not an earning event --- No basis

adjustment

- EITF Topic D-102 Documentation

- The hedging instrument

- The hedged item

- The nature of the risk being hedged

- Prospective and retrospective effectiveness tests

- Post-Enron meltdown of energy trading sector

- Credit downgrades will affect fair value measurements

- Tighter watch on what qualifies for hedge accounting

- Netting of Financial Contracts --- http://www.mccannfitzgerald.ie/legal_briefing/banking_financial_services/netting_protection.html

One objective of risk management in the context of

derivatives transactions is to reduce overall credit risk, by using netting

agreements to set off the market value of gains and losses on transactions.

Netting agreements provide for the termination of the transactions in specified

circumstances (including insolvency circumstances), provide a mechanism for

valuing the lost economic value and related termination costs of the terminated

transactions and aggregate those individual values/costs to a single net sum.

Only the net sum arising is then payable. Without netting, in an insolvency

situation, a non-defaulting party may have to pay in full in respect of the

out-of-the-money transactions whilst, as an ordinary creditor, receiving little

or nothing in respect of the in-the-money transactions.

FAS 143 --- Accounting for Asset Retirement Obligations

- The new rule requires businesses to record the fair value of a liability

for an asset retirement obligation in the period in which it is incurred.

When the liability is initially recorded, the entity capitalizes a cost by

increasing the carrying amount of the related long-lived asset. Over time,

the liability is accreted to its present value each period, and the

capitalized cost is depreciated over the useful life of the related asset.

Upon settlement of the liability, an entity either settles the obligation

for its recorded amount or incurs a gain or loss upon settlement.

- Measure the liability at fair value

- Methodology will be a change for many oil and gas companies

- Most do not discount the liability and recognize accretion expense

- Most do not measure the liability at fair value

- Many do not gross up the balance sheet (i.e., the liability is

embedded in accumulated depletion, depr., and amortization (DD&A)

- Many assume salvage value of surface equipment will offset reclamation

costs

FAS 146 --- Accounting for Costs Associated with Exit or Disposal

Activities

- This Statement addresses financial accounting and reporting for costs

associated with exit or disposal activities and nullifies Emerging Issues

Task Force (EITF) Issue No. 94-3, "Liability Recognition for Certain

Employee Termination Benefits and Other Costs to Exit an Activity (including

Certain Costs Incurred in a Restructuring)."

- The Board decided to address the accounting and reporting for costs

associated with exit or disposal activities because entities increasingly

are engaging in exit and disposal activities and certain costs associated

with those activities were recognized as liabilities at a plan (commitment)

date under Issue 94-3 that did not meet the definition of a liability in

FASB Concepts Statement No. 6, Elements of Financial Statements.

- The principal difference between this Statement and Issue 94-3 relates to

its requirements for recognition of a liability for a cost associated with

an exit or disposal activity. This Statement requires that a liability for a

cost associated with an exit or disposal activity be recognized when the

liability is incurred. Under Issue 94-3, a liability for an exit cost as

defined in Issue 94-3 was recognized at the date of an entity’s commitment

to an exit plan. A fundamental conclusion reached by the Board in this

Statement is that an entity’s commitment to a plan, by itself, does not

create a present obligation to others that meets the definition of a

liability. Therefore, this Statement eliminates the definition and

requirements for recognition of exit costs in Issue 94-3. This Statement

also establishes that fair value is the objective for initial measurement of

the liability.

- Applies to costs of terminating contracts and closing or consolidating

facilities

EITF 98-10 --- Rescinded

Reversal of mark-to-market gains on certain energy contracts to reflect the

rescinding of Emerging Issues Task Force (EITF) Issue No. 98-10, “Accounting

for Contracts Involved in Energy Trading and Risk Management Activities”

- Non-derivatives no longer marked to market (e.g., storage contracts,

tolling agreements, capacity contracts, inventory)

- Fair value accounting model for inventory challenged

- Disclosures no longer required

- Valuation and disclosure to be taken up later by the FASB

FIN 45 --- Guarantor’s Accounting and Disclosure requirements for

Guarantees, Including Indirect Guarantees of Indebtedness of Others

The Interpretation should significantly improve the reporting of guarantees

that are issued in conjunction with other transactions, such as when a seller

also guarantees its customer’s repayment of the funds borrowed to pay the

seller for the customer’s purchases.” This guidance does not apply to

certain guarantee contracts, such as those issued by insurance companies or for

a lessee’s residual value guarantee embedded in a capital lease. The

provisions related to recognizing a liability at inception of the guarantee for

the fair value of the guarantor’s obligations would not apply to product

warranties or to guarantees accounted for as derivatives.

Ceiling/Impairment Tests

• Accounting Standards IAS 36, FRS 11 and FAS 121

Accounting For Decommissioning/Site Restoration

• Accounting Standards IAS 37, FRS 12, and US GAAP

Impact Of Accounting Policy Choices

Analysis Of Oil And Gas Company Financial

Statements

Financing Arrangements

• Accounting for farm ins/farm outs and carried interests

Sales Revenue Accounting

• Accounting for overlift and underlift

• Accounting for take or pay sales agreements

Pending Revision of FAS 123

Stock Options

If the FASB and the IASB require expensing of stock options when vested rather

than exercised, it will have really adverse effects on the bottom lines of some

companies who rely heavily upon employee stock options for compensation.

This is why the U.S. House and Senate are already gearing up for a fight with

the FASB and possibly SEC due to heavy lobbying pressures. In the March

31, 2003 issue of Barron's on Page 28, the following sample impacts are

provided:

|

Adjusting Earnings for Options

»Earnings of major tech

companies are well below reported levels when adjusted for option

grants to employees. Options will become a big issue next year when

companies likely will be forced to record them as an expense. Some

companies, like Microsoft, are reducing option grants, helping

shareholders.

|

| Company |

Microsoft |

Intel |

IBM |

Cisco |

Oracle |

Applied

Materials |

EMC |

Hewlett-Packard |

Texas

Instruments |

| Recent Stock Price |

$25.04 |

17.58 |

81.45 |

13.5 |

11.36 |

13.5 |

7.16 |

16.44 |

17.75 |

| 2002 Earnings* |

$0.92 |

0.51 |

3.95 |

0.39 |

0.41 |

0.19 |

-0.05 |

0.79 |

0.22 |

| Option-adjusted'02 Profits* |

$0.71 |

0.34 |

3.28 |

0.19 |

0.33 |

0 |

-0.22 |

0.48 |

-0.01 |

| 2002 P/E Ratio |

27.2 |

34.5 |

20.6 |

34.6 |

27.7 |

67.5 |

NM |

20.8 |

80.7 |

| 2002 Option-adjusted P/E |

35.3 |

51.7 |

24.8 |

71.1 |

34.4 |

NM |

NM |

34.3 |

NM |

| 2002 Options Grant (mil) |

82 |

174 |

60 |

282 |

63 |

9 |

52 |

66 |

37 |

| Options Grant Relative to Shares

Outstanding |

0.8% |

2.6 |

3.5 |

3.8 |

1.2 |

0.5 |

2.4 |

2.2 |

2.1 |

| Options Issuance Trend |

ä |

ä |

ã |

ä |

ä |

ä |

ä |

ã |

ã |

| *2002 Fiscal Year.

NM-Not meaningful.

Sources: Company reports; Thomson/Baseline |

See Bob Jensen's letter to Senator

Charles E. Schumer --- http://www.trinity.edu/rjensen/theory/sfas123/jensen01.htm

(Includes updates not sent to Senator Schumer)

S&P Core Earnings Theory --- http://www.trinity.edu/rjensen//theory/00overview/CoreEarnings.htm

"Bubble Redux," by Andrew Bary, Barron's, April 14, 2003,

Page 17.

Amazon's valuation is the most

egregious of the 'Net trio. It trades for 80 times projected "pro

forma" 2003 profit of 32 cents a share. Amazon's pro forma

definition of profit, moreover, is dubious because it excludes re-structuring

charges and, more important, the restricted stock that Amazon now is issuing

to employees in lieu of stock options. Amazon's reported profit this

year under generally accepted accounting principles (which include

restricted-stock costs) could be just 10 cents to 15 cents a share, meaning

that Amazon's true P/E arguably is closer to 200.

Yahoo, meanwhile, now commands

70 times estimated 2003 net of 35 cents a share, and eBay fetches 65 times

projected 2003 net of $1.35 a share.

What's fair value? By our

calculations, Amazon is worth, at best, roughly 90% of its projected 2003

revenue of $4.6 billion. That translates into $10 a share, or $4.1 billion.

This estimate is charitable because the country's two most successful

brick-and-mortar retailers, Wal-Mart Stores and Home Depot, also

trade for about 90% of 2003 sales.

Yahoo ought to trade closer to

15. That's a stiff 43 times projected 2003 earnings and gives the

company credit for its strong balance sheet, featuring over $2 a share in cash

and another $3 a share for its stake in Yahoo Japan, which has become that

country's eBay.

Sure, eBay undoubtedly is the

most successful Internet company and the only one that has lived up to the

growth projections made during the Bubble. As the dominant online

marketplace in the U.S. and Europe, eBay saw its earnings surge to 87 cents a

share last year from three cents in 1998, when it went public at a

split-adjusted $3.00 a share.

Why would eBay be more fairly

valued around 60, its price just several months ago? At 60, eBay would

trade at 44 times projected 2003 profit of $1.35 a share and 22 times an

optimistic 2005 estimate of $2.75. So confident are analysts about

eBay's outlook that they're comfortable valuing the stock on a 2005 earnings

estimate.

Fans of eBay believe its profit

can rise at a 35% annual clip in the next five years, a difficult rate for any

company to maintain, even one, such as eBay, with a "scalable"

business model that allows it to easily accommodate more transactions while

maintaining its enviable gross margins of 80%. If the company earns $5 a

share in 2007--nearly six times last year's profit--it would still trade at 18

times that very optimistic profit level.

Continued in the article.

Bob Jensen's threads on pro forma earnings are at http://www.trinity.edu/rjensen//theory/00overview/theory01.htm#ProForma

Equity Valuation

Bob Jensen's Threads on Return on Business Valuation, Business Combinations,

Investment (ROI), and Pro Forma Financial Reporting --- http://www.trinity.edu/rjensen/roi.htm

|

Questrom vs. Federated Department Stores, Inc.: A Question of Equity

Value," by Gary Taylor, William Sampson, and Benton Gup, Issues in

Accounting Education, May 2001, pp. 223-256.

This is perhaps the best short case that I've ever read. It will

undoubtedly help my students better understand weighted average cost of capital,

free cash flow valuation, and the residual income model. The three student

handouts are outstanding. Bravo to Taylor, Sampson, and Gup. If you

subscribe to the electronic option of the American Accounting Association, you

can download the case from http://aaahq.org/ic/browse.htm

The market value

represents the firm’s stock price at a given point multiplied by the number of

shares outstanding. The intrinsic value

of the firm is the present value of the forecasted payoffs of income, cash flow,

or other economic variables to the stockholder; thus, the intrinsic value

represents the value implied by avail-able information. The intrinsic value is

the theoretical value of the firm based on any one of a variety of valuation

methods such as free cash flow,

residual income, or dividend

discount. Consequently, wide variation can exist in

estimates of a firm’s intrinsic value.

During the 1980s, a significant amount of research

suggested that financial markets are informationally efficient. However, in

recent years, research has re-vealed many market imperfections. Size and

seasonality effects temper the assumption that stocks are fairly priced at any

given time. In addition, Wall Street spends a considerable amount of time and

money on identifying “mispriced stocks,”

Market Value

Market value is only indirectly affected by limited and/or misleading financial

reports. Traders and investors can look at all other sources of

information setting bid and ask prices. However, only a small proportion

of shares are usually traded and these seldom reflect the value of enormous

blocks of equity, especially blocks that provide ownership control of

management. Also, daily stock prices are heavily influenced by general

market conditions and trends that may be poorly correlated with changes in value

in a particular company. Also daily stock prices are impacted upon by

accounting data news releases that are subject to all the limitations of

accounting data used in computing intrinsic values.

Intrinsic Value

Intrinsic value suffers most from more direct reliance upon what

accountants report in the way of earnings, cash flows, and account

balances. The main limitation is the valuation impact of items not

accounted for such as intellectual capital, quality reputation, brand

recognition, political power/connections, monopoly power, and other

intangibles. Another major problem is that management compensation

contracts contribute to misleading and/or fraudulent manipulation of the

accounting numbers. Further complications include impacts of

extraordinary items in financial statements and early extinguishment of

debt. Enormous problems arise from complicated and obscure

measurement and disclosures under such unfathomable accounting standards

like FAS 133 on Accounting for Derivative Financial Instruments and

Hedging Activities. Many disclosure footnotes such as the infamous

Footnote 16 of the Enron 2000 annual report cannot be understood by top

experts --- http://www.trinity.edu/rjensen/fraud.htm#Senator

- Discounted Dividend (DD)Valuation:

In theory, the best economic value is the present value of all

future cash flows (dividends) on each share of common stock.

Since many firms do not pay dividends or pay miniscule dividends,

the ability to pay a dividend must be used as a surrogate for

dividends. This in turn leads to the FCF surrogate described

below.

- Free Cash Flow (FCF)

Valuation:

"Free cash flow" is the amount of cash remaining from

operations after cash is used

for new investments. It is the cash theoretically avail-able to

pay bondholders and shareholders. It is calculated as the sum of

"net cash provided

from operating activities," after adding back after-tax net

interest payments, less

(plus) "cash used for (generated from) investing

activities." The resulting amount

is the cash available to pay bondholders or shareholders, i.e.,

"free cash

flow."

- FCF is not a true measure of value created since cash outflows

for investing activities reduce FCF. However, as long as the

company is not investing in negative NPV projects, investing

activities should increase firm value. Problems with the FCF

model are evident for firms whose FCFs have not reached a steady

state. For these firms, it is difficult to predict the timing of

future investing activities, making it difficult to predict

expected future free cash flows. If these firms are successful,

they will ultimately incur positive free cash flows, but only in

the future, when returns from their investment are

realized.

- Wal-Mart illustrates the problems associated with using the

FCF model to estimate the intrinsic value of a firm whose FCFs

have not reached a steady state. From 1988 through 1996,

Wal-Mart’s FCFs were positive only in 1989. The negative FCF

amounts during these years were due to the large outflows of

cash used to expand its retail stores; these outflows for

investing activities exceeded Wal-Mart’s operating cash flow.

Despite its negative FCFs, Wal-Mart’s price per share

increased from $6.875 in 1988 to $20.375 in 1996. In addition,

Wal-Mart notes in its 2000 annual report plans to expand in

international markets, thereby making additional negative free

cash flows likely for the foreseeable future. Yet the price per

share continues to increase.

- Residual Income (RI) or "Abnormal Earnings"

Valuation:

“Residual Income” is the earnings above “normal earnings.”

“Normal earnings” are the required earnings expected by

investors, given the cost of capital, and is calculated by

multiplying the beginning-of-the-period book value of equity (Bt–1

) by the firm’s cost of capital (r). Mathematically, residual

income for period t is from forecasted eps estimates (fepst

– rBt–1 ) where fepst is forecasted

earnings for period t. Residual earnings are also called “abnormal

earnings.”

Residual Income Model:

The “Residual Income” (RI) model is a valuation tool that is

derived directly from the discounted dividend model. The RI model

estimates intrinsic value by looking at both “stocks” (balance

sheet equity amounts) and “flows” (earnings). The RI model

estimates a firm’s total equity value as a function of the book

value of common equity and the present value of residual income. The

mathematical relationship between per-share forecasted earnings,

share price, and book value is: P0 = B0 +

Sum[(1 + r) –t (feps t – rB t–1 )], where P0

and B0 represent today’s price per share and book value

per share of equity, respectively. Cost of capital is defined as r

and forecasted earnings per share as “feps.”

Federated's

Valuation Estimates Using the Free Cash Flow (FCF) Model

Subtracting Deferred Taxes

Table 1

on Page 251 when the share price on January28, 1995 was $18.625

| |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

| Discount

Rate |

No

Perpetuity

1995-1999 |

Perpetuity |

Growing

in Perpetuity |

| 5% |

$(30.80) |

$93.22 |

$279.26 |

| 10% |

$(33.15) |

$18.34 |

$40.40 |

| 15% |

$(35.07) |

$(

6.34) |

$

0.84 |

|

Federated's

Valuation Estimates Using the Residual Income (RI) Model

Table 2

on Page 252 when the share price on January28, 1995 was $18.625

| |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

Intrinsic

Value (IV)

Per Share |

| Discount

Rate |

No

Perpetuity

1995-1999 |

Perpetuity |

Growing

in Perpetuity |

| 5% |

$23.33 |

$62.64 |

$121.59 |

| 10% |

$19.37 |

$27.24 |

$30.61 |

| 15% |

$16.21 |

$15.89 |

$18.81 |

|

The share price on April 3, 2003 was $28.50. There are no

dividends.

|