|

A Presentation by Rashad Abdel-Khalik

|

Caveat: . I am grateful to Professor Abdel-Khalik for allowing me to videotape his inspiring presentation. The quotations from Professor Abdel-Khalik that appear at various points in this document have never been edited by him. However, since he is my good friend I took the liberty of making some editorial clarifications at points where he massacres the King's English. My videotape was transcribed by my secretary, Debbie Bowling. I prefer to minimize changes in the transcription so that what is read remains as close as possible to what the audience listened to at the conference. None of us speak with the formalized vocabulary and grammar used in our writing. Also we cannot edit what we said in the same manner that we can edit what we wrote. Bob Jensen added notes in red text.

TENTH ASIAN-PACIFIC CONFERENCE ON

INTERNATIONAL ACCOUNTING ISSUES

SESSION 2(B), October 26, 1998

Review of SFAS 133 Derivative Financial Instruments Accounting

Rashad Abdel-Khalik

Graduate Research Professor, University of FloridaTable of Contents

Introduction by Rashad Abdel-Khalik

SFAS 133 Cannot Account for Complex Related Hedgings

SFAS 133 Inconsistently Treats Identical Transactions Differently (Between Contracting Parties)

Concluding Remarks By Gary Sundam

Bob Jensen's SFAS 133 Glossary and Transcriptions of Experts

Introduction by Gary Sundem (University of Washington)

The last presenter is Rashad Abdel-Khalik. He's the Graduate Research Professor at The University of Florida. That's not an impressive sounding title, but I think it's probably one of the most prestigious chairs that any school in the U.S. Rashad is very well respected. He has a Ph.D. from The University of Illinois, has taught at Columbia, Duke and Illinois before moving to Florida, as well as visiting positions elsewhere, and probably most of you got to know him when he was Editor of The Accounting Review for four years I think. During that time and since then has been an international traveler and been at many of these meetings and I always find Rashad interesting to listen to. And we're going to hear from Rashad about some hedging issues, and you've heard all positive things about the reporting of financial instruments. I think Rashad may have a few things on the other side to share with us --- Rashad.

Review of SFAS 133 Derivative Financial Instruments Accounting

Rashad Abdel-Khalik

Graduate Research Professor, University of Florida

I'd like to raise four points. The presentation made by the previous speakers, Hamid and Walter, were very interesting and very informative, and I would like to agree with them except to the points that I want to make. I apologize for smaller print than it should've been.

I want to say why firms hedge. Why do firms hedge? The reason that I want to say that we all know that, why firms hedge without --- mention briefly simply because I want to leave you a point at the end which relates to graphics I will share to you.

The second point is I wanted to say a little bit about the impairment complexity of the standard and of hedging process. And then I will go into the SFAS 133 that Hamid talked about, and I want to show you my view of SFAS 133. There are several views of it, but I'll raise only two issues. One is that the same transactions or the same activities can be treated differently under SFAS 133. And SFAS 133 has questions on transactions basics to the extent that we are unable to determine the success or failure of the hedging activities. So SFAS 133 does not help in achieving the purpose intended, and it's an extremely complex standard. And then finally the fourth point is that it gives opportunities for management to manage by intent --- to account by intent. That is, accounting is based on what the management thinks --- in terms of what it thinks --- has and that is related to the qualifying criteria that Hamid has mentioned.

So, in order to get into these points here let's first take up why firm is hedged. There are several hypotheses and the finance literature is full of those hypothesis and research on that. And basically three main hypothesis that arise; one is taxes --- to minimize the taxation burden across countries. And that second one is to hedge executive compensation. Someone recently looked at mining companies in particular and found out that the percentage of common shared ownership, by shareholders and by executives, is a major determinant of whether or not managers engage in hedging. And the third reason of course, if you would have derivatives that are not hedging, you are speculating under the disguise of hedging. It blames hedging, and what they are frankly doing is speculating. And the Long Term Capital Management fund is an example of that --- that's the best example. LTCM was a big speculation, and they called it hedging.

Primarily hedging is made in order to manage risk, usually to reduce risk. That's the primary objective of hedging. We want to reduce risk. And I'll give you what I call simple-minded examples to help understand this for me, and then highlight the points I'm getting to. The risks we're talking about price risk. The risk of price changes. So the objective hedging has reduced the exposure of the firm to the fact that they may lose by having a higher cost or by having to pay a higher debt, or a higher exchange rate. So there are three important price risks --- the change in commodity prices, the change in interest rates, and the change in exchange rates. So what the objective of hedging is to reduce the firm's exposure to possible loss when they're exposed to any one of these price risks.

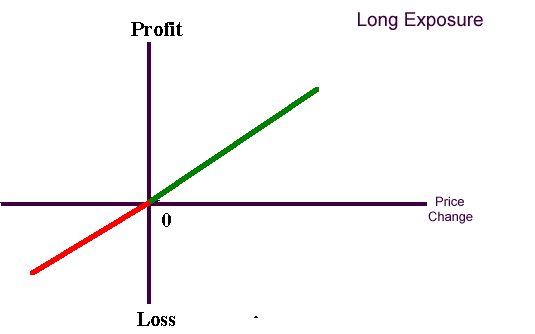

To give you an example of hedge purchased for simplicity here, let's assume that the form here this graph here gives us an idea about this exposure.

|

This graph on the vertical axis, that is the change in the value of the firm. On the horizontal axis it is the change in the price. The price can be any price that we talked about. It can be the change in the price. The change in price can be the change in interest rates or price interest rate, exchange price or commodity price. Suppose this profile here is a line that presents the risk exposure from the firm. That is, if the price goes up, you gain. If the price goes low, you lose. That's the long exposure. That is to say that if you buy stock and the price of the stock goes you up you gain. And if the price of stock goes down, you lose.

Suppose you want to neutralize your exposure to that risk? So to neutralize your exposure to that risk, you just take another activity which will counter that. And so as a result you wipe out that exposure, and you end up with an expectation --- you end up with expected loses here. Remember all of this is done in expectation. That is, after it happens you may actually end up losing more, you may gain more but before you made that activity of hedged or hedging [unsure], the object is to be --- is to neutralize the expexposure so we don't lose or gain. An example: let's take for example the first price that we're talking about, the oil produced. An oil producer that's a commodity price risk. If the price of oil goes up the oil producer will gain from the value of the increase. The price goes down the oil producer will lose. That's the risk that's involved of this oil producer.

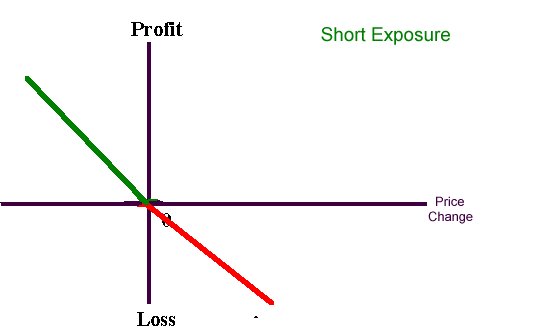

If you look at an airliner that uses oil, the risk for is opposite that of the oil refiner. If the price goes up, the airline will lose; if the price goes down the airline would make more profit. So this is the risk for file the airline. Price goes down they gain; price goes up they lose. So now each one of these wants to reduce the risk exposure for different reasons. The oil producer wants to reduce the risk exposure in the negative region. The refiner does not want to hedge exposure of profit --- right? The oil refiner want to use risk exposure of loss. So the oil refiners might engage in options --- correct? Or they engage in a series of transactions of swaps, forward contracts, and futures such that the combination of the net of those transactions or derivatives becomes eliminating any expectation or the possibility in the future of the exposure to the negative risk, the downside risk.

|

Similarly the airline is not going to eliminate the exposure to the profit side when the price goes down. So they get engaged in the using the risk exposure to the negative region, to the loss. And so they engage in a different positions from that of the refiners' forwards contracts or futures contracts.

As a second example consider a simple swap --- interest rate swap. This company has $200 million loan at a fixed rate of 5%. Assume that operating revenues from cash flows in this company vary directly with interest rates --- if interest rates increase revenues increase and vice versa. And so the company is exposed to the risk that if the cash flows go down, the company cannot afford the risk of being short of cash to pay its 5% fixed loan payments of $10 million per year. So that's the risk exposure to the possibility that the cash flow may not cover 5%. So what they do, the go do a counterparty; a dealer or somebody else that in a swap will accept fixed payments of $10 per year in exchange for variable rates that could be less than or greater than the $10 million.. The variable rate on the $200 million can be based on LIBOR --- London Inter-bank Rate.

SFAS 133 Cannot Account for Complex Related Hedgings

Note from Bob Jensen: At this point Rashad presents a real world Mexcobre illustration reported by Paul B. Spraos. I liked his example so well that I created a separate document explaining the example in somewhat greater detail than Rashad could cover in his presentation time allowed in this session in Maui. Click here to view the Mexcobre illustration.

Rashad. The (Mexcobre) case I gave you is a real case; it's a real story; it's not made up. This was published in the journal Corporate Finance. What's happened is the loan of $210 million from ten banks --- this is the first cash flow transaction that took place. The ten banks loaned Mexicana de Cobre (Mexcobre), a producer of copper, $210 million.. Now the banks are exposed to two things --- political risk and commodity risk of that the copper price --- the price of copper will go down and the company will not be able to pay. So what the banks involved engaged in a set of multiple transactions. They said we want to reduce the downside risk, you know the negative region, the loss.

Click here to view the Mexcobre illustration.

So the banks now get from this escrow account 11.48% every year capped. If the price of copper creates a surplus in the escrow account, the surplus is returned to Mexcobre. The escrow account is exposed to change in the spot price of copper on the London Mercantile Exchange (LME), and therefore the ten banks receiving funds from the escrow account want to hedge this account against copper price risk. So what the the New York bank did is go to Banque Paribas and enter into a copper price swap. The escrow fund receives a fixed at $2,000 per ton from Banque Paribuas in a swap for the floating LME copper price based upon copper spot rates.

Note that this is a very complicated process. There are several swaps, there are several commodity prices used as variable. Interest rates involved and three countries are involved. And there is foreign currency risk involved of these transparencies.

Question/Comment. And different instruments.

Rashad. And different instruments, yes. So now this gets back now --- we don't need to understand the details of these particular transactions but let me go back now to the main point that I want to raise. Remember Walter talked about that, yes?

Question/Comment. Somebody has to accept that risk involved if the price of copper goes down. Somebody will take a loss.

Note from Bob Jensen: This is a very good question. I raise the question and provide a solution in my answer key to this case. Click here to view the Mexcobre illustration.

Rashad. Well that's distributing the risk in some ways. Everyone's trying to reduce their own risk exposure and shift risk to somebody else who's trying to reduce risk positions by shifting something to somebody else.

So that the question that I'm trying to get at here is the following: Suppose we are the FASB and the Security Exchange Commission here in the United States. When looking at these banks we are telling them report the value at risk that you're exposed to from this derivative. This swaps do not qualify as a hedge under the SFAS 133 --- correct? Because they're not clearly-and-closely related to to qualify as hedges. It's very indirect ,and so it did not change the value of this loan on the balance sheet. It stays at historical cost. Now this hedge here exposes these ten banks to risk.

Suppose the SEC asks the banks to produce the value at risk. There are only two models for value at risk that are being used in the financial community. One is by J. P. Morgan, which is based on multi-purpose relations in a very extensive model. And J.P. Morgan sells this for a huge sum of money to banks. Chase Manhattan Bank also has a VAR model selling for a very high price, and it's not transparent. So measuring value at risk is an extremely complex process --- correct?

When the Mexcobre case is viewed as one transaction, note that the risk at these banks are exposed is not from one swap, it's from this swap and this swap, and this dealing of copper price exchange. Commodity risk, copper price risk, and foreign currency risk are all involved.

How do you measure the value at risk? There's no way! The risks at these banks are exposed to extends beyond the simple, simple swap that these banks are showing here. There is no all out admission to exposure of these things to risk. So the fact that then we report value at risk in this case we are over-simplifying the process extremely. Now the controller general director said at one time, a year ago, that on any day and GE is not a financial institution, on any day GE has 1200 forward contracts. Now these are extremely complex to account for in aggregate. So that's one issue that we get to.

SFAS 133 Inconsistently Treats Identical Transactions Differently Between Contracting Parties

Example 1 (Interest Rate Swap)

The second problem that I had with SFAS 133 lies in treating the same activities differently both parties to a contract. Let's take a simple example. Let's take a swap, interest rate swap in which ABC Company receives fixed-rate loan interest and pays a variable rate on a notional amount, say $1 billion to XYZ Company. And XYZ receives that floating rate London Bank Inter-Bank (LIBOR) rate plus a swap increment and pays out a fixed rate. This is one contract. One side is called ABC and the other side is called XYZ. Under SFAS 133, ABC will consider that a fair value hedge and XYZ will account for it as a cash flow hedge the same activity. The accounting asymetry, according to the FASB's logic, is that what ABC's trying to hedge a change in fair value of the asset and XYZ declares it is hedging the cash flow.

Note from Bob Jensen: This illustration from ABC's standpoint is accounted for as shown in Example 2 in Appendix B of SFAS 133 in Paragraph 115 on Page 63. It is not at all clear to me that XYZ can account for the swap as a cash flow hedge unless XYZ has another contract in which XYZ pays out exactly the same variable amount it receives from ABC Company. In this way XYZ could be hedging its variable rate cash flows from the loan obligation. In this instance, XYZ would have to declare its swap with ABC as a hedge against its variable rate loan. Only the effective portion of the hedge would qualify for income deferral postings to other comprehensive income. Something like XYZ's cash flow hedge is illustrated in Example 6 of SFAS 133, pp. 76-79, Paragraphs 140-143.

But is this really an inconsistency or asymetry of accounting for ABC versus XYZ. ABC's fair value hedge is self contained in its swap with XYZ? From XYZ's standpoint it is not even a hedge unless there is another contract that is being hedged. I am not sure what point Rashad is really trying to make here since it is not the same "hedge" for ABC as it is XYZ.

In any case, the accounting in XYZ's case is no obvious without added information about management intent when declaring hedge accounting. See Paragraph 28 in SFAS 133 commencing on Page 18.

Rashad. For ABC, a gain or loss from the fair value hedge goes into current earnings. For XYZ, it goes into a garbage can called other comprehensive income --- which is a suspense guy sitting there. If you don't know, throw it there, right? And maybe later on when you know, you put back to income. That's what it is, right? And so the same assets is recorded here at fair value goes up and down with the market the recorded here at historical cost, which stays the same. That's ridiculous.

Question/Comment. But you don't have the same asset.

Rashad. Well, that's --- that's debatable, correct?

Question/Comment. But they have the swap but the two companies don't have the same underlying.

Question/Comment. No, that's it, they don't have the same swap.

Rashad. They don't have the same underlying asset.

Question/Comment. But one has a risk exposure.

Rashad. The point I'm making here is if you value all assets and all liabilities at fair value you do not have this nonsense. You don't have this mess that we have there --- correct? Why put that in the net swap cash inflow or outflow for ABC in current income and defer the same net amount in other comprehensive income for XYZ?. If you have all assets value at fair value we don't have that problem.

Question/Comment. But you suggested that to anyone that is doing accounting, their reaction would be even more [faded].

Rashad. I know, I know. But that's exactly what Gary Sundem stated at the beginning of this session. We have a (historical cost) model that's dead, and we are just adding to it. We are stitching things to it. So it doesn't work.

Question/Comment. I bet the FASB would argue this is the first step you've got to take.

Rashad. Oh yes, sure, sure. But I'm talking about it from my point of view. And you agree with me on that. Do I have time, how much time?

Example 2 (Foreign Currency Hedge of Firm Commitment)

Let me take another case that is bothering to me. Let's take a case of an importer. The importer is importing from Germany. The U.S. importer is faced with a possible gain or loss on a firm purchase commitment that has not yet been settled. If the price of the Deutsche mark goes up, then you lose --- right? The importer has to pay more in dollars even though the Deutsche mark price remains unchanged. If the price goes down the importer wins. He has to do this in dollars. In order to neutralize currency exchange risk, the importer then has to get engage in some kind of hedging activity. And that activity can be entering into a forward contract. And the forward contract would pay you if the price goes down and you pay them if the price goes up. So you neutralize the firm commitment --- foreign currency risk exposure becomes zero. All gains and losses on the forward contract can be deferred in comprehensive income until the purchase transaction takes place.

Note from Bob Jensen: To see the accounting for this forward contract, Example 3 of SFAS 133, Page 67, Paragraph 123.

Suppose you combine a forward contract and an option, so that you only neutralize the down side risk. So you can have a mixed of an instrument to eliminate your exposure to the downside risk with a forward contract and pay an option premium in order to benefit from upside currency movements --- right? SFAS 133 says that if management declares the forward as a cash flow hedge, hedge and this is the asset to be hedged. But forecasted transactions now it's a forecasted transaction and you treat it in the following way, right?

Note from Jensen: I completely missed Rashad's point here. The accounting seems relatively clear under SFAS 133. The forward contract is accounted for as illustrated in Example 3 of SFAS 133, Page 67, Paragraph 123.. The option contract is then accounted for as illustrated in Example 9 of SFAS 133 in Paragraphs 162-164.

A related type of situation is a swaption formed by the combination of a swap and an option.

Question/Comment. It's a firm commitment?

Rashad. It's a firm commitment, and yes any gain on the option goes to current income.

Now let's take another case. Suppose the company doesn't want the hedge this way.

Note from Bob Jensen: Here Rashad gave a rather confusing hedging alternative that I will try to simplify it with my own similar illustration. In the above example, suppose that we have a German subsidiary called SUB. What we can do is make our German SUB a loan with ultimate principal plus interest equal to the firm commitment prices of the imported goods. The SUB can immediately convert the loan from U.S. dollars into Deutsche marks prior to settlement of our firm commitment. In this manner we do not have to enter into a derivative contract to effectively hedge against any exchange rate movements. We have a "psuedo forward" contract that does not have to be recorded as a forward contract under SFAS 133. Since the prices imported items remain unchanged in Deutsche marks, we can simply have SUB ultimately purchase the items and ship them to us in the U.S. for full repayment of the loan. For simplicity assume the loan principal plus interest earned by the SUB (prior to the purchase transaction) equals the purchase price.

Rashad. So we have in essence sort of hedged in the real way --- right? This is exactly the same kind of hedge that a forward contract would give us. The latter "hedge" is not considered by SFAS 133 as a hedge of a derivative instrument. And so what they do, this parent would have to record this loan at historical cost. If you have forward contract, you have account for it at fair value as a fair value hedge or a cash flow hedge depending upon management intent. So why are we treating the forward hedge versus the psuedo forward hedge differently? They serve the same purpose.

Question/Comment. Are you translating it into U.S. Dollar? [Faded]

Rashad. There's no loss to them at the currency exchange. But the debts or assets are recorded at historical cost and the accounting for hedging forward contract is not treated the same way as this one here (the psuedo forward).

So the other thing that bothers me is that how do you identify success in managing risks? Right now what we do is that every time --- so if you have fair value hedge. Every time things change you add it to asset and subtract from income or --- subtract from asset and add it to income --- right?

Question/Comment. It washes out?

Rashad. It washes out, but now suppose, for example, I'm buying an asset from Germany, and I hedge. I have a fixed commitment. I'm buying a machine. I hedged the foreign currency exchange with a forward contract. The gain or loss on that forward contract goes to the value for the asset and will be be charged over the years of depreciation. So I'm spreading now the gain or loss over the years. So in some cases the income shows the gain or loss; in some cases the gain or loss is spread over time and some cases goes to the garbage can that is called other comprehensive income instead of current income. If you get the end result of SFAS 133 and look at the annual report, you could never tell whether the management has been successful in managing financial risk or not. Can you tell from the outcome of SFAS 133 whether a company's succeeded or failed in managing financial risk? No, I cannot, because the information about managing financial risk is spread everywhere and distributed every where.

If you buy inventory and you hedge the price of inventory, the gain or loss in that hedge goes to the price of the inventory. So I don't know now from the disclosure how much of the cost of goods sold was the presenting success in hedge or failure in hedge and how much was really the activity.

Question/Comment. You're not allowed to participate in sales profits, so in other words you're not allowed to take gains as profits from the sell of inventory. The inventory still stays in historical cost.

Rashad. Inventory stays at historical cost? What would ---? You have to adjust ---

Question/Comment. [Unsure] Given the other liability forward contract.

Rashad. It has to be adjusted.

Question/Comment. Increase the asset; increase the liability or vise versa.

Rashad. It is compensated somewhere there, but I manage with for inventory and someone else doesn't. The numbers are produced do not reveal to me how much of it is managed --- is financial risk management and how much is not. That's the point I'm trying to make. Ok, so I can go on more on that but ---

The last thing is management by intent. Managers tell us that a derivative is intended to serve as a specific hedge. Next month, they change their minds. It is no longer a hedge and becomes a speculation. Accounting for a derivative's speculation is really straightforward. If you gain, it goes to income; if you lose, it goes to income as a loss --- right? And you acquire fair value. But if you say I'm using this as a cash flow hedge, it may not go to income

Many of these things are values at risk, and all these reports are at one point in time when we all know how fluid these things are. Future contracts are settled every day. You have to --- at the end of the day, the trading exchange has to find out the net difference and settle, transfer money from one to the other. Well companies could have changed their position within a minute before 12 o'clock midnight, and next minute they had very highly risky business in derivatives and it doesn't show.

We need to show the pattern of activity over time, how much risk exposure have you exposed to stockholders or the firm over the period not at one point in time it makes no sense. And we don't have that added from SEC or SFAS 133.

Thank you.

Concluding Remarks by Gary Sundam

Thank you Rashad. Let me just summarize one thing relating to hedging that --- I guess I sit here listening to all of this in kind of a finance perspective. If we had completed perfect capital margins, there would be no reason to hedge. If I'm an investor, what I really want to know is do these hedges create completeness in the capital market or do they change the transactions cost that are involved? Would I be better as an investor to hedge myself in my portfolio of investments, or do I want the firm to incur those transactions cost to hedge for me? I would like to know something about the transactions cost that are involved in the hedging of a firm and I guess to me --- and I'm certainly not an expert in this, but I don't see that coming out any place in these kind of disclosures. And so what I see is a lot of hedging going on, not because it hedges the shareholders but because it hedges the managers. And to some extent I'm not sure I want that from a shareholders perspective to defer that kind of hedging, I would at least like to disclose how much that hedging is costing.

And so I think there's another whole dimension to some of these disclosures that really hasn't been dealt with yet. And I have no idea how to deal with them, but on that point I think we're past our time. I would like to thank our panelists, I think they've done a great job of dealing with a very complex issue clearly in the limited time that we've had.

Bob Jensen's SFAS 133 Glossary and Transcriptions of Experts