$251 Million Loan for 38 Months at 11.48% APR |

|

Mexcobre

Case

The Real World Case of a Controversial Accounting

for a Copper Swap that Challenges SFAS 133

Bob Jensen at Trinity University

Source: This case is rooted in a review of a real world copper swap reported by Paul B. Spraos in "The Anatomy of a Copper Swap," Corporate Risk Management and on "Mexcobre Loan Deal Repays Debt," Corporate Finance, August 1989. It is reproduced in Managing Financial Risk: A Guide to Derivative Products, Financial Engineering, and Value Maximization by C.W. Smithson, C.W. Smith, Jr., and D.S. Wilford (Chicago: Irwin Professional Publishing). These earlier references did not address accounting issues. The case has been modified somewhat in minor ways. The answers were prepared on the basis of a $251 million loan.

Acknowledgement: I am grateful to Rashad Abdel-Khalik for making me aware of this illustration during his presentation at the Tenth Asian-Pacific Conference on International Accounting Issues, Maui, October 26, 1998. Rashad sent me a photocopy of the Spraos article. I then wrote this Mexcobre Case for my students in ACCT 5341 in International Accounting Theories.

Table of Contents

Case Presentation and Answer Spreadsheets

Why do companies enter into interest rate swaps?

How did Sogem from Belgium hedge political risk?

How did a copper swap hedge copper price fluctuation risk?

Case Questions and Assignments

Click Here to Request Bob Jensen's Solutions to the Mexcobre Case

Bob Jensen's SFAS 133 Glossary and Transcriptions of Experts

Presentation Displays for the Mexcobre Case

Bob Jensen at Trinity University

Link to this file of the case and short answer summaries: http://www.trinity.edu/rjensen/caseans/133spshow.htm

Link to the case without answers: http://www.trinity.edu/rjensen/acct5341/133cases/133sp.htm

Link to the 133spans.xls Excel workbook that has the complete answer sheets:http://www.cs.trinity.edu/~rjensen/13300tut.htm

Link to the SFAS 133 and IAS 39 Glossary: http://www.trinity.edu/rjensen/acct5341/speakers/133glosf.htm

Links to related cases: http://www.trinity.edu/rjensen/acct5341/133cases/000index.htm

$251 Million Loan for 38 Months at 11.48% APR |

|

Excel Workbook of Answers to Mexcobre Case Questions

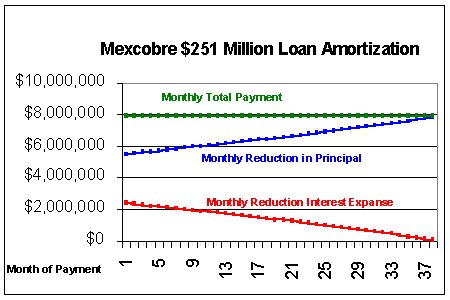

Amortization Schedule for $251 Million Loan

How did swaps reduce copper price fluctuation risk?

Shortly after Salamon Brothers invented the interest rate swap financial instruments derivative in a contract between IBM and the World Bank in 1981, this type of derivative was used to manage risk in a copper mining operation in a Mexican company called Mexicana de Cobre (Mexcobre), a subsidiary of a copper mining group in Mexicao called Group Mexico. The transaction eventually involved ten banks in several nations, a Belgian customer, multiple foreign currencies, and Mexcobre itself.

Why do companies enter into swaps?

In a simple (plain) vanilla swap, the purpose is usually to swap variable rate interest obligations for fixed-rate obligations. The firm with variable rate debt can often swap for a better deal than can be obtained directly on a fixed-rate loan. Reasons for this can be complicated. Sometimes it is a matter of timing. For example, when a firm acquires variable rate debt, that type of debt may appear to be the best deal. With the passage of time, the firm may change its preference toward fixed-rate debt. Negotiating an interest rate swap may have lower transactions cost than paying off the variable rate debt and refinancing with fixed-rate debt. The counter party in the swap, on the other hand, may be willing to speculate or otherwise prefer to swap for variable rate payments.

In more complex situations, there may be capital market inefficiencies that make interest rate swaps advantageous. Firms enter into swaps to either speculate or to hedge interest rate risk. In some instances, fixed-rate debt cannot be obtained directly at any rate. For example, suppose a company has low or even zero credit standing in a certain nation and negotiates to swap interest payments with a company that has high credit standing in that nation. Swaps are often brokered by international banks of high credit standing that eliminate credit risk of both parties to a swap. In any case, swap cash flows are usually netted against each other so the default risk would be low even if there were no payment guarantees. Direct loans often entail credit risk, especially if the borrower is from one nation and the lender is from another nation. Interest rate swaps account for over 70% of all financial instrument derivatives contracts. The reason is that they are a means of reducing credit risk, transactions costs, and market risk in hedging and speculating contracts.

The Mexcobre copper exporting subsidiary of Groupo Mexico faced such enormous financial price risks that it was effectively denied access to international debt markets. At the same time, it was paying a burdensome 23% interest rate to the Mexican Government. Through a complex international swap arrangement, Mexcobre managed to replace its high cost $251 million debt with a 11.48% fixed-rate interest payment that equates to 0.9567% per month.

|

How did Sogem from Belgium hedge political risk?

A crucial part of the case came in reducing political risk in Mexico. Since so much labor is involved in copper mining, the Mexican government is not likely to take drastic measures or impose taxes that impede the mining and sale of copper. However, the government might impede cash flows. For example, suppose the Mexican government chooses to tax or otherwise impede interest payments going to the ten banks outside of Mexico in an effort to protect its own loans to Mexican companies. The ten outside banks hedged against such political risk by avoiding cash payments from Mexico. This was accomplished with a purchase contract in which a firm called Sogem in Belgium agreed to purchase nearly 4,000 tons of copper each month at spot rates on the London Mercantile Exchange (LME). Payments, however, went into an escrow account in a New York Bank. These funds, in turn, were used to service $251 million loaned to Mexcobre by ten banks.

|

How did a copper swap hedge copper price fluctuation risk?

If copper prices plunged, there was a possibility that the balance of funds in escrow in New York would not be sufficient to service the debt on the $251 million in loans to Mexcobre by ten banks.

|

The Bank in New York controlling the escrow account acted at the request of the ten lending banks to hedge against copper price movements. Banque Paribus was willing to swap with the escrow fund for variable copper prices and guarantee a fixed monthly price or $2,000 per ton on 4,000 tons per month.

The contract with Mexcobre capped the return of the New York Banks to 0.9567% per month. Any excess cash from high copper prices above the capped loan rate were returned to Mexcobre.

Question 01

Discuss the various types of risks faced by the ten banks if they simply loaned $251

million to Mexicana de Cobre (Mexcobre) at a fixed interest rate and did not engage in the

other contracting mentioned in the case. Discuss both direct and indirect risks.

Do not assume any Sogem or Banque Paribus hedging when answering this question.

[Hint: See the term "risk" in Bob Jensen's SFAS 133 Glossary at http://www.trinity.edu/rjensen/133glosf.htm ]

| Political Risk | ||

| Default Risk (Credit Risk, Natural Disaster Risk, Labor Strife) | ||

| Foreign Currency Risk if loan is in pesos | ||

| Refinancing Risk if Interest Rates Plunge | ||

| Opportunity Loss Risk if Interest Rates Soar | ||

Question 02

Why was Sogem in Belgium hedging contract demanded by the ten banks? Ignore the copper

price swap with Banque Paribus when answering Question 2.

Are the hedged items (i.e., the fixed interest payments on the loan to Mexcobre) firm commitments or forecasted transactions? Answer in terms of the notional, underlying, and disincentive for nonperformance on each loan payment.

What implications does this have for the note being a hedged item under Paragraph 21d or 29e of SFAS 133? Can the Sogem hedge affect Other Comprehensive Income (OCI)?

| Political risk of Mexican taxes and cash outflow restrictions |

| With payments at 4,000 tons of copper, the receivable is a cash flow hedge |

Notional = 4,000 tons Underlying = copper price. |

| Case mentions no disincentives, but clearly Mexcobre would lose credit standing worldwide if loan is defaulted. |

| See my solution for the discussion of Paragraphs 21d and 29e. |

Question 03

Does the net effect of all this transacting result in fixed-rate or variable-rate loan to

Mexcobre? Explain your answer in terms of when it is a fixed-rate loan versus when

it is a variable-rate loan. Also explain the importance of whether

"excess" interest revenues are returned to Mexcobre.

| Copper price swap + return of of excess cash | Loan rate is fixed at 11.48% APR |

| No copper price swap | Loan rate is variable |

Question 04

After all the contracts in this case are signed, what risks have been assumed by both

Banque Paribus and Sogem in Belgium? How can these risks be hedged by Sogem and Banque

Paribus? You may assume derivatives not mentioned in this case as well as those mentioned

in the case. Explain your answer.

| Banque Paribus assumed the copper price fluctuation risk on 4,000 tons of copper per month. |

| Sogem in Belgium must buy 4,000 tons per month at spot prices no matter what its needs. |

Question 05

In Question 1, you discussed the various types of risks faced by the ten banks if they

simply loaned $251 million to Mexicana de Cobre (Mexcobre). Aside from transactions costs

in arranging all the contracts (especially the Sogem contract and the Banque Paribus

contract), what risks remain to justify charging 11.48% to Mexcobre rather than a much

lower interest rate since political risks and copper price risks have been hedged?

In other words, why wouldn't the loan be attractive to U.S. banks for 8% which, for

example, might be the lending rate to a copper mine in Montana?

| New York banks assume risk of Mexcobre not sending 4,000 tons per month New York banks assume risk of default by Sogem in Belgium and Banque Paribus Legal jurisdiction risks in Mexico, Belgium, and Bahamas |

Question 06

Can the copper price swap with Banque Paribus be accounted for as a cash flow hedge using

SFAS 133 accounting rules? Is the copper price swap to "clearly and closely

related" to the contract with Sogem? In addition to SFAS 133 standard criteria

for cash flow hedges, add an explaination of your position as to whether this constitutes commodity-indexed interest and principal payments in the

context of SFAS 133.

[Hint: See Paragraph 61i on Page 43 of SFAS 133.]

| With respect to Paragraph 61i of SFAS 133, note that the loan servicing payments are constant at $7,909,666 in the Sheet 3 amortization schedule. These do not vary with any commodity prices. Therefore, Paragraph 61i should not block a cash flow hedge that assures each payment. |

Question 07

In Question 7 and all remaining questions, assume that all

ten banks comprise what is called the "New York Bank." You may then

account for transactions within only that one bank.

In Question 7 and all remaining questions, assume the New York Bank closes its revenue and expense accounts to Retained Earnings at the end of each month.

For this question, assume there is no $251 million loan to Mexcobre. Instead, you may assume that the bank has some type of income from Sogem that is paid in cash each month equal to the LME spot price of copper multiplied by 4,000 tons each month. In other words, pretend for now that the New York Bank can retain all cash flows from its swap contract with Banque Paribus. Assume the New York Bank in this instance chooses to account for the copper swap as a cash flow hedge under SFAS 133 (ignoring any argument that SFAS 133 might not apply). You are to make journal entries for only the copper price hedge between the New York Bank and Banque Paribus. Ignore the fact that ten banks are involved and assume all net swap payments flow to or from the New York Bank. Also ignore arguments such as those given in Question 2 that the note may not qualify as a hedged item under SFAS 133 criteria for hedged items.

What is the journal entry made by the New York Bank at the date the swap is initiated on January 1, 19x1? What is the entry made on January 31, 19x1 by this bank to record the cash payment from Sogem in Belgium for 4,000 tons of copper at $1,850 per ton? Limit your answer to the swap accounting and do not attempt to account for loan of $251 million in this question or the return of any surplus payments to Mexcobre. Assume that in the first month, the Banque Paribus honors its swap obligation by sending the New York Bank a check for the net difference between $2,000 per ton versus the spot price of $1,850 per ton for 4,000 tons of copper. What is the journal entry for the New York Bank to account for the swap payment? What are the journal entries for Banque Paribus at the inception of the swap on January 1, 19x1 and after the first net swap cash payment on January 31, 19x1?

Assume the books are closed at the end of each month and show the closing entry to Retained Earnings as well as the closing balance in retained earnings assuming no other transactions.

Repeat the January 31 entries for February 28 and March 31 net cash flows from both the Sogem and Banque Paribus contracts. Accumulate the balances for Cash, Other Comprehensive Income, and Retained Earnings from the January 31 balances. Assume that the LME copper spot prices are $2,100 for February and $2,400 for March on 4,000 tons of copper each month.

When making the SFAS 133 journal entries for the swap, use the data in the following table:

Month |

Current Copper Price/ton |

Swap Receivable Price |

Net Price Difference |

Journal Entry Date |

Copper Swap Cash Flow |

Assumed Swap Value |

| 01/01/x1 | $0 | |||||

| 1 | $1,850 | $2,000 | $150 | 01/31/x1 | $600,000 | $16,942,276 |

| 2 | $2,100 | $2,000 | ($100) | 02/28/x1 | ($400,000) | ($11,064,274) |

| 3 | $2,400 | $2,000 | ($400) | 03/31x1 | ($1,600,000) | ($43,320,951) |

In Question 7, restrict your entries to cash flows from Sogem and the SFAS 133 entries for the copper price swap. Entries for the Mexcobre note will be made in a later question.

Please use the following Chart of Accounts in your journal entries:

Cash

Copper price swap receivable/payable

Interest expense/revenue (this account is not used in Question 7)

Loss/gain on copper price speculation (use this account for all cash flows in Question 7)

Other comprehensive income

Retained earnings

To view the answer to Question 7, you must click here and scroll to the answer.

The main conclusion to Question 7 is that the New York Bank in this instance has a copper price exposure risk on spot price movements of 4,000 tons of copper per month. Over the first three months, the speculation gain turns out to be $8,000,000.

Question 08

Now you are to return to the case involving the loan to Mexcobre and the copper price

swap.

Please derive the $251 loan amortization schedule across for a fixed-rate of 11.48% APR or a 0.9567% fixed monthly rate for 38 months. In a spreadsheet, show the interest expense, principal reduction, and total loan payment each month that is deducted from the cash payments from Sogem and Banque Paribus. Also show the "excess" cash each month if the copper price swap yields $8.0 million each month to service the amortized sum of the principal and interest portions that total $7,909,666 each month. Discuss why the loan would probably not be periodically remeasured to market value under SFAS 115 rules. Why might this not affect having to remeasure the copper price swap to market value on the books of the bank?

Click here to view the loan amortization schedule.

If there is sufficient cash available each month, loan service payments are $7,909,666 prorated between interest revenue and principal reduction. If $8,000,000 is received each month from the copper price swap, the remaining $90,344 is returned to Mexcobre each month.

Question 09

Compute the breakeven price of copper for which the New York Bank will exactly earn its contracted 0.9567% per month. Then comment on the impact of varying copper prices when surplus funds above the breakeven copper price are returned versus not returned to Mexcobre.

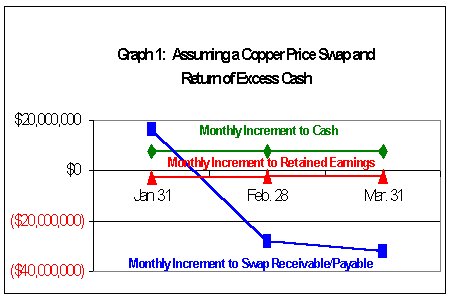

Please draw two graphs comparing the monthly increase in cash versus the monthly increase in retained earnings for January 31, February 28, and March 31. Also show the pattern of the change in the value of the copper price swap beside the changes in cash and retained earnings from these transactions. You only need to graph the first three months.

Graph 1: Assume a copper price swap with a return of cash flows in excess of $7,909,666 per month.

| Graph 1: Assuming a copper price swap and a return of excess cash | ||||||

| Change in Balance | Jan. 31 | Feb. 28 | Mar. 31 | Balance | ||

| Cash | $7,909,666 | $7,909,666 | $7,909,666 | $23,728,998 | ||

| Swap receivable/payable | $16,942,276 | ($28,006,550) | ($32,256,678) | ($43,320,951) | ||

| Retained earnings | ($2,401,233) | ($2,348,536) | ($2,295,335) | ($7,045,104) | ||

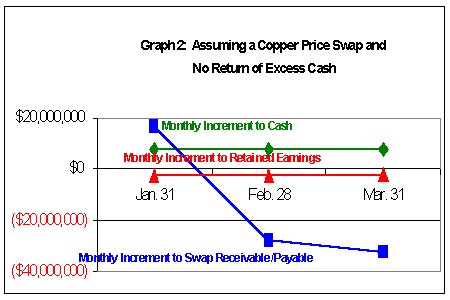

Graph 2: Assume a copper price swap with no return of cash flows in excess of $7,909,666 per month.

| Graph 2: Assuming a copper price swap and no return of excess cash | ||||||

| Change in Balance | Jan. 31 | Feb. 28 | Mar. 31 | Balance | ||

| Cash | $8,000,000 | $8,000,000 | $8,000,000 | $24,000,000 | ||

| Swap receivable/payable | $16,942,276 | ($28,006,550) | ($32,256,678) | ($43,320,951) | ||

| Retained earnings | ($2,491,577) | ($2,438,880) | ($2,385,679) | ($7,316,136) | ||

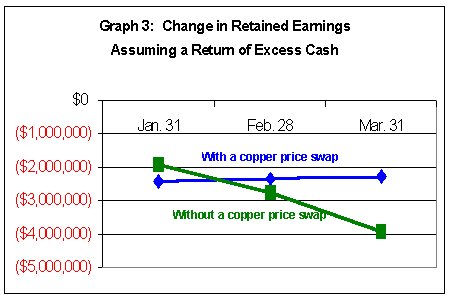

Please draw two additional graphs comparing the monthly retained earnings balances with versus without a copper price swap. Assume the copper prices given in Question 7.

Graph 3: Change in Retained Earnings with versus without a swap and return of cash flows in excess of $7,909,666 per month.

| Graph 3: Change in retained earnings assuming a return of excess cash | |||||

| Change in RE Balance | Jan. 31 | Feb. 28 | Mar. 31 | Balance | |

| With price swap | ($2,401,233) | ($2,348,536) | ($2,295,335) | ($7,045,104) | |

| Without a price swap | ($1,891,568) | ($2,748,536) | ($3,895,335) | ($8,535,439) | |

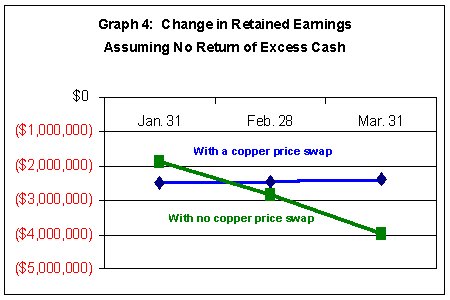

Graph 4: Change in Retained Earnings with versus without a swap no return of cash flows in excess of $7,909,666 per month.

| Graph 4: Change in retained earnings assuming no return of excess cash | |||||

| Change in RE Balance | Jan. 31 | Feb. 28 | Mar. 31 | Balance | |

| With price swap | ($2,491,577) | ($2,438,880) | ($2,385,679) | ($7,316,136) | |

| Without a price swap | ($1,891,568) | ($2,838,870) | ($3,985,669) | ($8,716,107) | |

At the end of your answers to Question 9, discuss whether this copper price swap was effective in terms of SFAS 133 criteria for hedge effectiveness. Explain your answer.

The copper price hedge is perfectly effective in hedging the cash flows from Sogem. It meets all effectiveness tests in SFAS 133. In maintaining a constant $8 million cash flow, however, the swap's value declines in February and March do to soaring prices of copper.

Question 10

For this question, assume that the one New York Bank loaned the entire $251 million to

Mexcobre under the terms spelled out in the case. In Question 10 you are to assume that

the copper price swap satisfies all SFAS 133 requirements to be a cash flow hedge of the

cash flows from Sogem in Belgium. Unlike in Question 7, assume that surplus funds from

high copper prices are returned monthly to Mexcobre above and beyond the 11.48% interest

rate that equates to 0.9567% per month. Also limit your answer to the contract to

loan $251 million, the contract between the New York Bank and Sogem, the contract with

Banque Paribus, and the return of surplus funds to Mexcobre. Assume that the loan

principal is amortized over 38 months much like mortgage note amortization in the

calculation of loan payments to the New York Bank at 0.9567%. In other words, each

net swap payment from the Banque Paribus is to be added to the Sogem payments. At

the end of each month, the New York Bank deducts a monthly loan payment from the fund

accumulated variable payments from Sogem and the net swap payments from Banque

Paribus. Any surplus is then sent to Mexcobre each month.

In summary, you are to make the New York Bank's journal entries for the following:

$251 million loan to Mexcobre on January 1, 19x1;

the Banque Paribus swap cash flow hedge contract on January 1, 19x1;

the variable monthly payments from Sogem on January 31, February 28, and March 31 assuming 4,000 tons per month at spot prices of $1,850 per ton in January, $2,100 per ton in February, and $2,400 per ton in March;

the monthly net copper swap receipts or payments from Banque Paribus on January 31, February 28, and March 31 on fixed swap receipts of $2,000 per ton and swap payments at the same prices used by Sogem to transmit the payments each month;

the first three loan payments (principal and interest) from the escrow fund to the New York Bank on January 31, February 28, and March 31, 19x1;

the three monthly surplus payments to Mexcobre in 19x1.

When making the SFAS 133 journal entries for the swap, please use the Question 7 data table.

Please use the following Chart of Accounts in your journal entries:

Cash

Copper price swap receivable/payable

Notes receivable - Mexcobre

Interest expense/revenue (this account is not used in Questions 7 and 8)

Loss/gain on copper price speculation (use this account only in Questions 7, 8, and 12)

Accounts payable - Mexcobre (in Question 10, any surplus funds are sent to Mexcobre monthly)

Even if surplus funds are transferred the same day they are received, please run them into

Accounts payable - Mexcobre and then settle the account in a separate entry.

Retained earnings

Hint: In Question 10 and Question 12, when cash is received from Sogem in Belgium, debit Cash and credit Accounts Payable - Mexcobre. When that payable is zeroed out each month, debit the payable and credit a combination of Interest Revenue, Notes Receivable, and Cash (for the excess cash sent to Mexcobre). In Question 10 when cash is received from Banque Paribus, debit Cash and credit Accounts Payable - Mexcobre. This is not an issue in Question 12 since there is no copper price swap with Banque Paribus in Question 12.

Question 10 Journal Entries Assuming Excess Cash is Returned Monthly |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Under SFAS 115 rules, the loan would probably be classified by the bank as a

security investment intended to be "held-to-maturity." A deal this complicated would be

difficult to classify as being "available-for-sale." In that case, the note receivable is not

remeasured to market on the balance sheet.

|

Question 11

Compute and compare the rate of return to the New York Bank in Question 10

for each of the first three months.

Compare this with the rate of return that would be obtained each month if the surplus funds were not returned to

Mexcobre. First assume the copper price swap is in effect and provide the rate of

return with or without return of cash flows above the 0.9567% per

month cap.

Next perform similar calculations assuming no copper price swap. In order to simplify the calculation of the rate of return with no copper price swap, compute each month's rate of return as the ratio of that month's net income from the Mexcobre transactions divided by the beginning balance of the note's principal still outstanding. You are to compare the solutions with versus without transfer of surplus funds to Mexcobre.

In summary, you are to provide answers in the following tables:

January of Year 1 |

Assuming the Interest Cap | Assuming No Interest Cap |

| Assuming Return of Excess Cash | ? | ? |

| Assuming No Return of Excess Cash | ? | ? |

February of Year 1 |

Assuming the Interest Cap | Assuming No Interest Cap |

| Assuming Return of Excess Cash | ? | ? |

| Assuming No Return of Excess Cash | ? | ? |

March of Year 1 |

Assuming the Interest Cap | Assuming No Interest Cap |

| Assuming Return of Excess Cash | ? | ? |

| Assuming No Return of Excess Cash | ? | ? |

Question 12

Repeat the January, February,

and March answers for Question 10 assuming that there is no copper price swap with

Banque Paribus. In order to simplify the calculation of the rate of return in Question 12,

compute each month's rate of return as the ratio of that month's net income from the

Mexcobre transactions divided by the beginning balance of the note's principal still

outstanding. You are to compare the solutions with versus

without transfer of surplus funds to Mexcobre. In other words, you must

provide two alternative sets of journal entries. Assume that the surplus funds sent

each month are either zero (if the copper price declines below the breakeven point) or

positive (equal to the surplus above the monthly breakeven point).

A major question here is whether to include the increments to Other Comprehensive Income (OCI) in the numerator of the rate of return calculations when surplus funds are not returned to Mexcobre. For Question 12, please add OCI increments to the numerator of the rate of return calculations.

Make all journal entries for the contracts with Mexcobre and Sogem. Assume that the note is maintained under amortized historical cost and is not adjusted for fair market value. Then compare all your journal entries for Question 12 versus Question 10. Please discuss the impact of the swap on the New York Bank.

After you finish the journal entries, compute the breakeven price of copper for which the New York Bank will exactly earn its contracted 11.48% per year or 0.9567% per month. Then comment on the impact of varying copper prices when surplus funds above the breakeven copper price are returned versus not returned to Mexcobre.

When making the SFAS 133 journal entries for the swap, please use the Question 7 data table.

Please use the same account names that are listed in the Chart of Accounts for Question 10.

In Question 12, assume that the Notes Receivable - Mexcobre account will always be credited with the loan amortization principal reduction from Question 10 no matter what the price of copper on the cash settlement date with Sogem in Belgium. In other words, all price fluctuations above and below the break-even price of copper affect interest revenue and cash settlements with Mexcobre. These price fluctuations do not affect the principal reductions on the note.

| Main conclusions given the note amortization

schedule given above.:

To obtain the contracted return of 11.48% per year, the New York Bank must receive exactly $7,909,666 according to the loan amortization schedule in Sheet 3. Hence the break even copper price is $7,909,666/4,000 = $1,977.42 per ton. If there is no copper price hedge and no surplus fund returns to Mexcobre, the New York will lose if copper prices fall below $1,977.42 and gain if they rise above $1,977.42. The bank had a copper price speculation loss in January since the $1,850 copper price fell below the $1,977.42 breakeven price per ton. In February and March it had relatively large copper price speculation gains from the high $2,100 and $2,400 prices per ton of copper at the LME spot prices. If surplus funds are returned to Mexcobre, the copper prices of $2,100 in February and $2,400 in March do benefit the New York Bank. However, if surplus funds are not returned, the New York bank now has a tough decision to make about whether it wants to speculate in copper price movements. In most instances, banks prefer to avoid such speculations. However, banks do not always avoid price speculations on such deals. As mentioned previously, however, the contract called for return of surplus funds to Mexcobre. Hence, the decision to hedge copper price movements that could never

benefit the New York Bank is a no-brainer for that bank. |

Question 13

From an accounting theory standpoint, do you think SFAS 133 accounting for the Mexcobre

transactions would help investors more easily analyze the risk management practices of the

New York Bank? (One bank was assumed in Questions 7-12 in order to simplify the case.)

If either the Sogem or the Banque Paribus contracts are booked and adjusted to fair value (no matter what the rules are under SFAS 133 or IAS 39), do you think that adjusting to fair value will help or hinder investor analysis of the New York Bank?

When answering this question, first present arguments on both sides of each issue. Then reason out your own conclusions.

Lastly, you are to discuss how the accounting would differ under IAS 39 versus SFAS 133.

| In Paragraph 220 on Page 123 of

SFAS 133, the FASB asserts that "fair value is the most

relevant measure for financial instruments and the only relevant measure

for derivative instruments." In that same paragraph, the FASB

claims "derivative instruments should be measured at fair

value, and adjustments in carrying amounts of hedged items should

reflect changes in their fair value (that is, gains or losses) that are

attributable to the risk being hedged . . ."

The analysis above for the Mexcobre Case vividly illustrates how not entering into a copper price swap would be totally stupid since the New York Bank(s) would only be exposed to losses due to copper price declines below $1,977.42 and would transfer all gains above that breakeven point to Mexcobre. Hence, the bank(s) did the entirely correct thing by entering into a copper price swap with Banque Paibus. In my viewpoint, the Mexcobre Case is a real world example of where SFAS 133 booking of the swap at fair value and adjusting that fair value each month is more misleading than helpful in this instance. I think there are many instances where following SFAS 133 rules leads to better accounting of derivative instruments. The Mexcobre Case, however, supports the arguments of bankers that applying SFAS 133 is not only difficult, it can be very misleading to investors when there is almost zero probability that the derivative instrument (a price swap in this case) will be held to the maturity. Maturity in this case is assumed to be the same maturity date as the date of maturity on the loan to Mexcobre. Unfortunately, SFAS 133 and its related SFAS 107 and SFAS 115 provide virtually no guidance for measuring fair value of contracts that are not traded in active markets or are traded in "thin" markets where a sparse number of transactions make market values unreliable as estimates of fair value. Like interest rate swaps and most other types of swaps, the swap contract with Banque Paibus is a custom-designed swap that is not traded in any market. No other contracts existed for 4,000 tons of copper per month across a 38 month horizon. The swap value estimates in Question 7, 10, and 12 are hypothetical and would be extremely difficult to estimate in the real world. Furthermore, the copper price movements around the $1,977.42 breakeven price create flip flops in disclosing the swap as a large receivable versus a large payable. For example, in January the copper swap is a large payable but becomes a large receivable in February and March. When prices decline below $1,977.42 it will flip flop back to a payable. What is bad for investors is that the flip flopping from being a receivable versus a payable is a signal that the bank(s) may be doing some type of speculating. In the Mexcobre Case, this could not be further from the truth. The bank(s) merely entered into a perfectly rational and stable price swap in order to prevent speculation losses and lock in a fixed return of 11.48% per year on the loan to Mexcobre. It would be irrational to terminate the swap before the loan terminates. Hence, the swap is not a trading item and reporting huge flip flops in value can only be misleading. In support of the bankers opposed to SFAS 133, reporting the changes in value as current earnings would be totally misleading in the Mexcobre Case. Disclosing these changes in OCI instead of earnings mitigates this problem, although I have to agree with Professor Rashad Abdel-Khalik that the OCI is merely a "garbage can" in this particular example if SFAS 133 rules are applied. An example of this same flip flop problem can be found in the FASB's own Example 5 beginning at Paragraph 5 on Page 72 of SFAS 133. You can read Dr. Abdel-Khalik's "garbage can" comments at http://WWW.Trinity.edu/rjensen/acct5341/speakers/133rasha.htm As indicated above, I support the SFAS 133 rules for many types of derivative financial instruments. However, the Mexcobre Case illustrates a real-world set of contracts for which SFAS 133 rules are dysfunctional. What is more upsetting is that standard setters around the world, including the International Accounting Standards Committee (IASC), are moving toward fair value accounting of all financial instruments with the corresponding changes in value being reported in (highly fluctuating) current earnings even for contracts such as the Banque Paibus copper price swap where there is no intention to terminate the swap until the Mexcobre loan terminates. Fluctuations in earnings due to fluctuations in value of such financial instruments creates a misleading instability in both income statements and balance sheets. Reporting value changes in OCI is only viewed as a temporary compromise with bankers until the standard setters eventually impose full value accounting in the extreme. At the time of this writing, it might be noted that the International Accounting Standards Committee (IASC) has its IAS 39 version of SFAS 133. IAS 39 allows designation of derivatives as trading versus non-trading for purposes of fair value measurement. The SFAS 133 does not allow such a distinction such that IAS 39 leads to better accounting for the Mexcobre case in my opinion if the swap is designated as non-trading under IAS 39. The December 1998 issue of the Journal of Accountancy provides an interesting contrast on fair value accounting. On Pages 12-13 you will find a speech by SEC Chairman Arthur Levitt bemoaning the increasingly common practice of auditors to allow earnings management. On Page 20 you will find a review of an Eight Circuit Court of Appeals case in which a firm prevented the reporting of net losses for 1988 and 1989 by persuading its auditor to allow reclassification of a large hotel as being "for sale" so that it could revalue historical cost book value to current exit value and record the gain as current income. Back issues of the Journal of Accountancy are now online at http://www.aicpa.org/pubs/jofa/joaiss.htm Note that at the time of the above lawsuit, available-for-sale investments were required to be adjusted to fair value with unrealized gains and losses being posted to current earnings. Subsequent to the lawsuit, SFAS 130 created Other Comprehensive Income for keeping such unrealized gains and losses out of current income unless the investment is reclassified as a trading investment rather than an available-for-sale investment. |

Bob Jensen's SFAS 133 Glossary and Transcriptions of Experts

For hedging via Eurodollar put options, see the CapIT Corporation Case.

For hedging via Eurodollar call options, see the FloorIT Bank Case.

For heding via Eurodollar futures contracts, see following cases: